Kimi: When Frontier Weights Become Open

On July 27, anyone with 1.4 terabytes of storage, 5TB of memory and a rack of accelerators will be able to run the world's third-most-intelligent AI system without paying its maker a cent.

The thesis in six lines

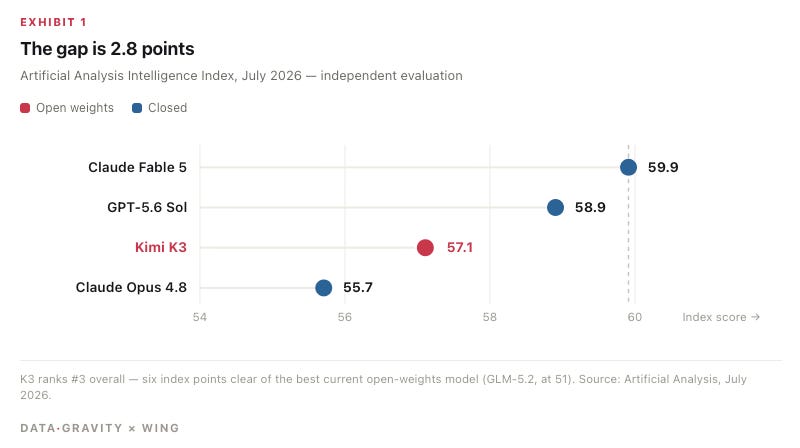

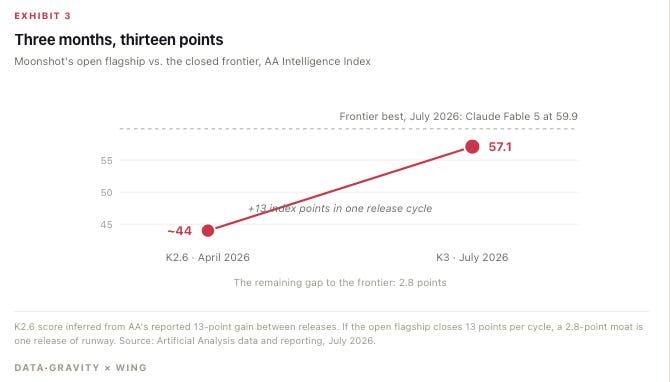

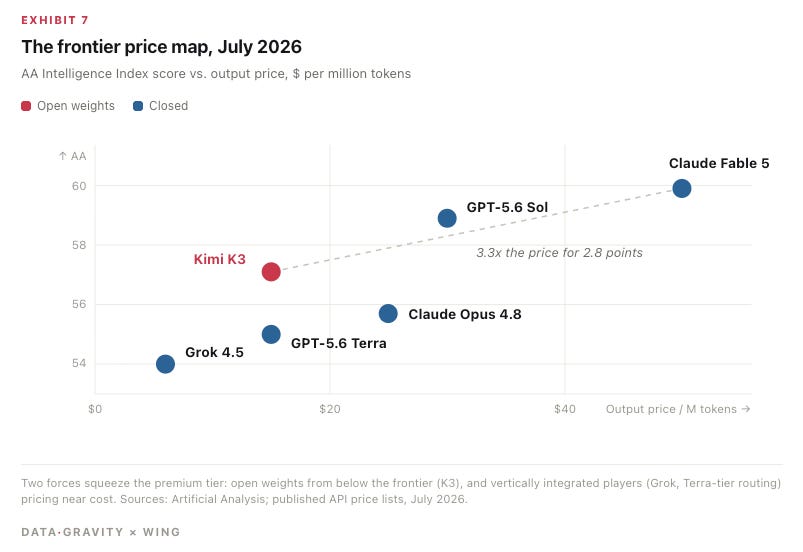

The frontier is no longer proprietary. Kimi K3 scores 57.1 on the Artificial Analysis Intelligence Index, #3 overall behind Claude Fable 5 (59.9) and GPT-5.6 Sol (58.9). The weights ship July 27. The last release cycle closed 13 points of gap in three months; 2.8 remain.

Margin gravity: closed labs run API gross margins estimated above 80%; open-model serving clears at ~40–45%. On a ~$250B 2030 inference market, that 35-point spread is ~$90B a year of margin migrating from model IP to compute and serving.

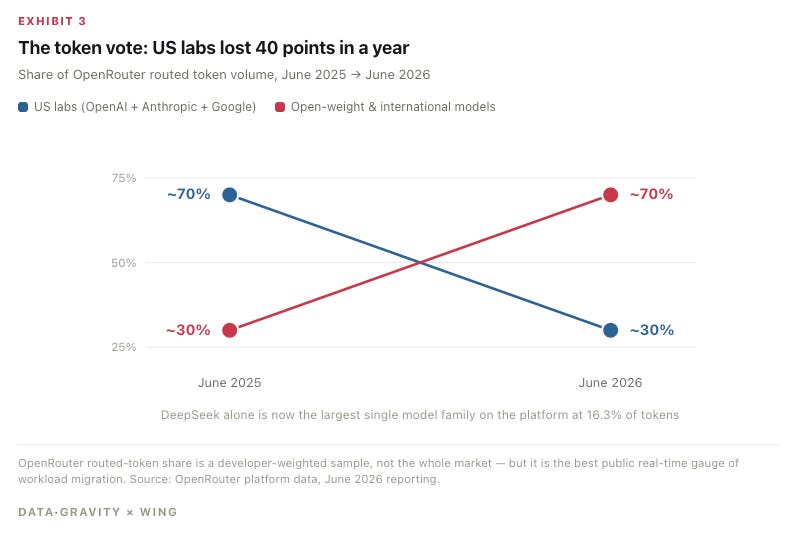

Bearish for labs: US labs’ OpenRouter token share fell ~70% → ~30% in twelve months. The moats that remain — product harnesses and internal checkpoints — are real, but nothing in the usage data prices them yet.

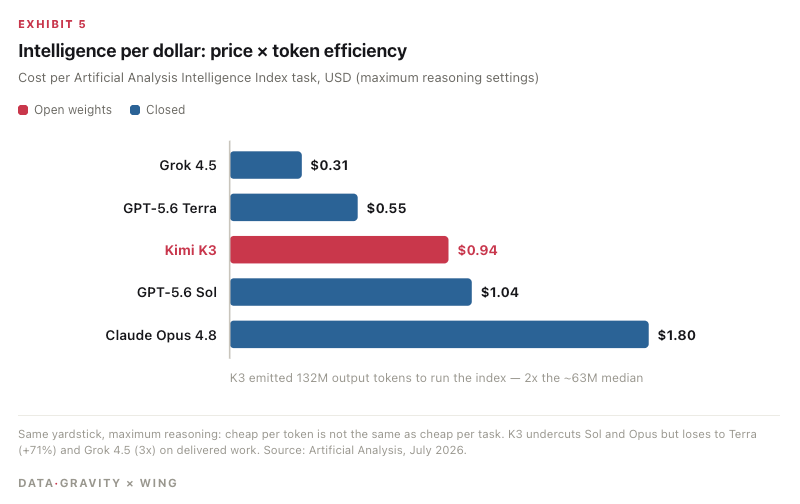

The caveat: K3 is a token wastrel: $0.94 per benchmark task vs. $0.55 for GPT-5.6 Terra and $0.31 for Grok 4.5. The true Sputnik is a token-efficient open frontier model. Not yet.

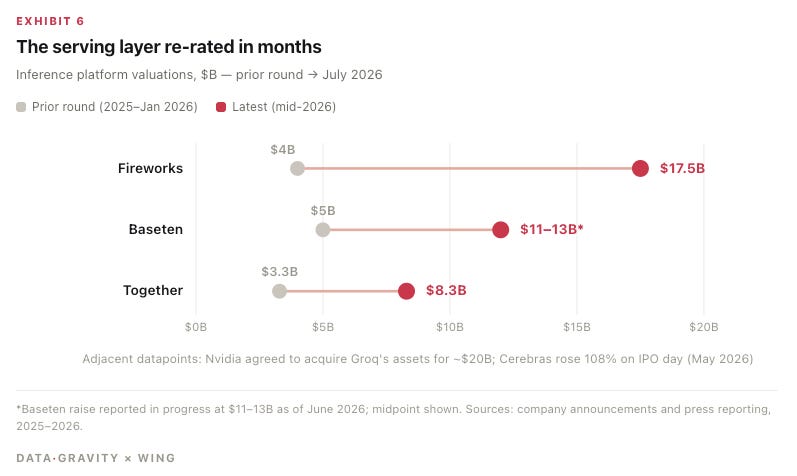

Bullish for compute, memory and serving: CoreWeave backlog $99.4B, Oracle RPO $638B, 2026 capex ~$725B — and export controls route open-model demand onto Western GPUs. Fireworks just repriced from $4B to $17.5B in seven months.

Five falsifiable calls at the end, starting with: K3 serves below $10 per million output tokens within 30 days of the weights dropping.

What Actually Shipped

The frontier became a file

imi K3 is a 2.8-trillion-parameter mixture-of-experts model: 896 experts, 16 active per token, roughly 50B active parameters, a 1M-token context window, weights trained natively in 4-bit precision. On Artificial Analysis’ independent index it scores 57.1, third overall behind Claude Fable 5 (59.9) and GPT-5.6 Sol (58.9). At launch it took #1 on the Frontend Code Arena at 1,679 Elo, above Fable 5’s 1,631 — the first Chinese model to top a major coding leaderboard.

The weights go public on July 27. That sentence is the entire story, because it converts the frontier from a service into a file. A service has pricing power. A file has distribution.

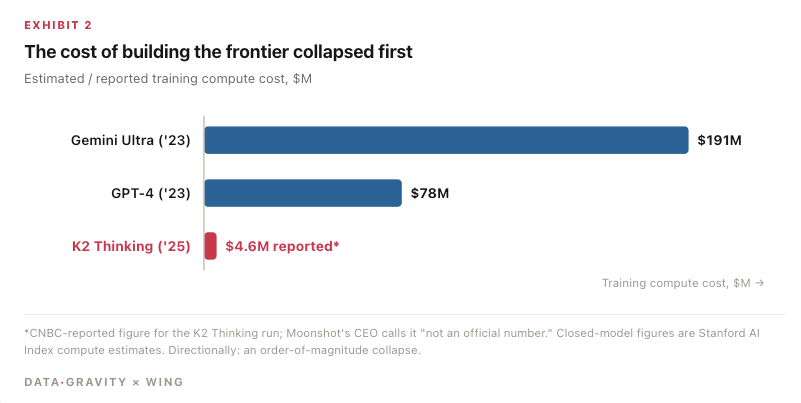

The producer economics explain why this keeps happening. Moonshot’s K2 Thinking was reported by CNBC to have cost roughly $4.6M to train — the company calls the figure unofficial — against Stanford-estimated compute costs of $78M for GPT-4 and $191M for Gemini Ultra. The velocity is the tell: six frontier-class releases in twelve months, ARR doubled from ~$100M to ~$200M in roughly six weeks this spring, valuation up from $2.5B in early 2024 to $20B in May with a $30B round reportedly forming ahead of a Hong Kong IPO.

K3’s price is its own signal. At $3 per million input tokens and $15 per million output, it costs more than 3x its predecessor. The era of super-cheap Chinese AI is ending. The era of free frontier weights is not — Moonshot is telling you open intelligence now clears at closed-tier prices.

Margin Gravity

Sizing the pool that moves

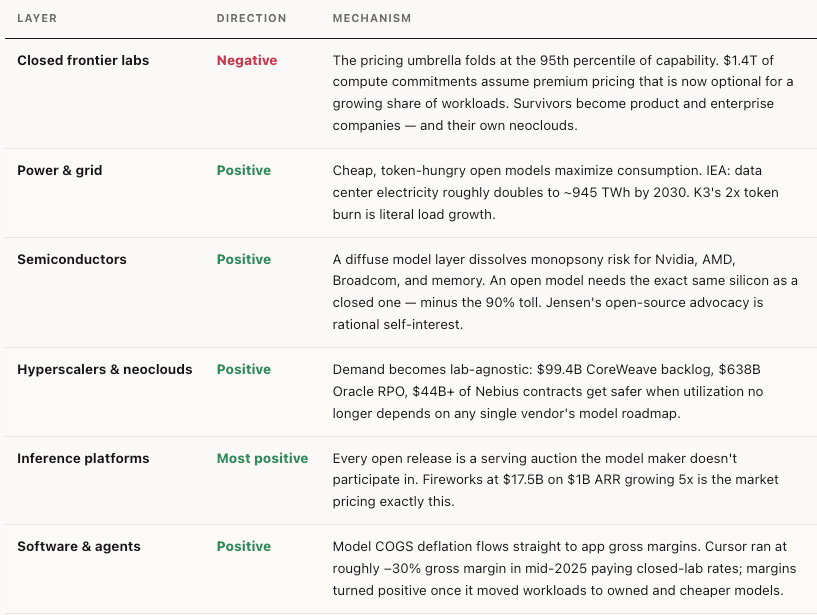

The cleanest frame for what K3 means comes from Gavin Baker. A world with two or three dominant frontier labs earning 90%+ inference margins is a world where those labs become monopsonies: the price-setting buyers of power, data centers, and semiconductors. They vertically integrate into every layer beneath them and subsume the application layer above. Awesome for those labs. Net negative for everyone else in the economy.

“A world where there are only 2–3 dominant frontier labs with 90% inference margins is net negative for every other layer while being awesome for those 2–3 labs… Anything that lowers margins and increases competition at the model layer is good for every other AI layer: power, semiconductors, hyperscalers, neoclouds and yes even software.”

Gavin Baker (@GavinSBaker), on Kimi K3 as “an important inflection point for AI,” X, July 2026

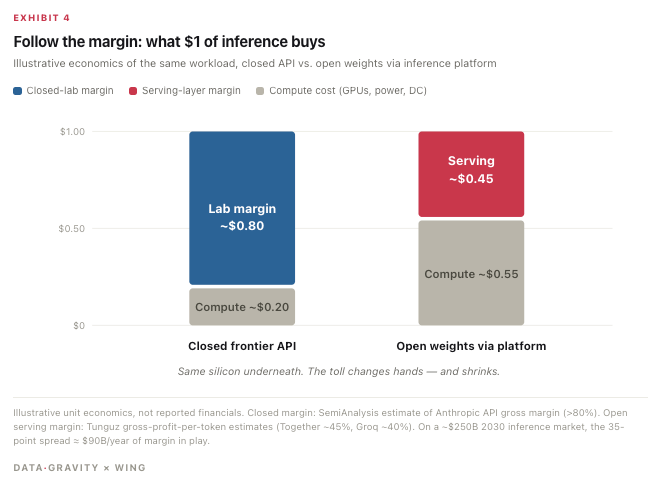

Now put numbers on it. The 90% figure is not hypothetical: SemiAnalysis estimates Anthropic’s API gross margins above 80%. When the same workload runs on an open model through an inference platform, the model toll disappears and the serving layer keeps an estimated 40–45% (Tom Tunguz pegs Together at ~45%, Groq at ~40%). The compute underneath is identical. Baker’s point, exactly: an open model requires the same silicon as a closed model of the same size and architecture. Only the toll changes hands.

Scale that spread. Forecasters put AI inference around $250B a year by 2030. On that base, every point of model-layer gross margin is $2.5B a year. The spread between an 80%-margin closed API and a 45%-margin open serving stack is 35 points: roughly $90B a year of margin that lands in compute, serving, and silicon instead of model IP — if workloads migrate. That is the pool K3 puts in play. Not revenue. Margin.

There are two roads to this repricing, and both are being paved at once. Open weights at the frontier is one: that is Moonshot. The other is vertically integrated players who don’t care where the margin dollars land: Grok 4.5 pricing output at $6 per million tokens, Meta’s Muse Spark 1.1 at $4.25, Gemini running on Google’s own TPUs. This is also why Jensen Huang champions open source, and it is not sentiment. A diffuse model layer dissolves the monopsony before it forms — and K3 is the first time the open road reached the frontier’s doorstep.

Bearish: The Labs

The frontier premium now depreciates in months

The closed labs sell exactly one thing at those margins: the gap between their best model and the best model you can download. That gap used to depreciate over years. K2.6 to K3 closed 13 index points in three months; 2.8 remain. The premium is still real. Its half-life is now measured in release cycles.

The market has been voting for a year. US labs’ share of tokens routed through OpenRouter fell from roughly 70% in June 2025 to ~30% in June 2026. DeepSeek alone is now the largest model family on the platform at 16.3% of volume.

Set that against the leader’s cost structure. OpenAI booked $13.1B of 2025 revenue against a reported $38.5B net loss, and carries $1.4T in compute commitments. That is a business that must defend premium pricing for a decade, at the exact moment premium pricing became optional for a growing share of workloads.

The labs’ own capital allocation concedes the point. OpenAI is designing 10GW of custom accelerators with Broadcom and bought 6GW of AMD supply. Anthropic contracted up to a million Google TPUs and committed $30B to Azure. Vertical integration is what you do when you expect the model layer’s margin to stop paying for the buildout.

Baker calls K3 only potentially negative for OpenAI and Anthropic. He grants them two outs, and both deserve to be taken seriously.

First, the product may now matter more than the model. Claude and ChatGPT are harnesses: memory, tooling, distribution, enterprise trust. Anthropic’s reported $47B run-rate is a workflow story sitting on top of models, not token resale — and it holds 61% of gateway spend on 32% of gateway tokens, which is what a working moat looks like. Second, the labs may hold internal checkpoints well ahead of anything public, compounding through recursive self-improvement. A few months of lead there could become permanent.

Both are real. Neither shows up in the direction of the usage data.

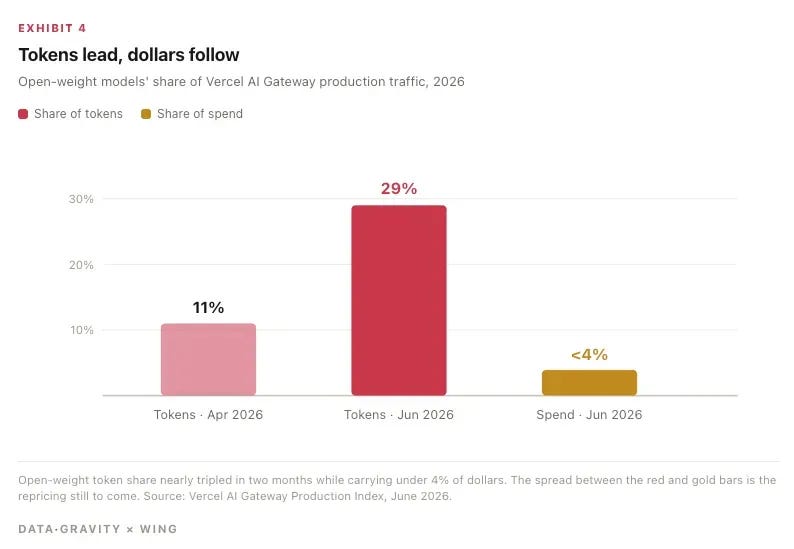

The dollars-versus-tokens gap is how you watch the race. Menlo Ventures put enterprise workloads at 89% closed at the end of 2025. Vercel’s gateway shows open-weight models carrying 29% of tokens and under 4% of spend, with token share nearly tripling in two months. Tokens lead. Dollars follow, unless the harness moat holds.

The Token-Efficiency Caveat

K3 is a token wastrel, and that cuts both ways

Intelligence per dollar is the product of two terms: price per token, and intelligence per token. K3 wins the first and loses the second.

It burned 132M output tokens running Artificial Analysis’ evaluation suite, more than double the ~63M median, because it ships with always-on maximum reasoning and no effort controls yet. The result is $0.94 per benchmark task: cheaper than GPT-5.6 Sol ($1.04), half of Claude Opus 4.8 ($1.80), but 71% above GPT-5.6 Terra ($0.55) and 3x Grok 4.5 ($0.31). The rough edges don’t stop there — K3’s hallucination rate on AA’s Omniscience test worsened to 51%, from K2.6’s 39%.

So the discount is real at the top of the closed stack and absent against its efficient tier. Running AA’s full index cost ~$2,700 on K3 versus ~$6,200 on Claude Fable 5, the most expensive model AA has ever benchmarked — but a closed lab routing to a token-efficient model at Terra’s price still undercuts the open alternative on delivered work. This is why Baker calls K3 an inflection point rather than a Sputnik moment. The true Sputnik is an open frontier model that is also token-efficient. It has not happened yet.

But inefficiency cuts both ways. Every wasted token is billed compute. A token-inefficient open model is a subsidy from Moonshot’s margin to whoever owns the GPUs it runs on.

Bullish: The Compute Layer

Free models are demand insurance for GPUs

A free frontier model destroys margin in exactly one place, the model API, and creates load everywhere beneath it. K3’s weights are ~1.4TB even at 4-bit precision. Moonshot recommends supernodes of 64 or more accelerators to serve them. Nobody downloads that onto a laptop.

This is Jevons operating at infrastructure scale. As the price of intelligence collapses, consumption explodes, and every unit of it clears through someone’s data center — including K3’s doubled token burn. Google now processes 3.2 quadrillion tokens a month, up 7x in a year. Inference has gone from a third of AI compute in 2023 to a projected two-thirds in 2026.

The operators are printing the evidence. CoreWeave grew Q1 revenue 112% to $2.1B with a $99.4B backlog. Nebius grew 684% and signed $17.4B from Microsoft and $27B from Meta. Oracle’s RPO hit $638B, up 363% year over year. Hyperscaler capex guidance for 2026 stands near $725B, up ~77%, against McKinsey’s $6.7–7T buildout estimate through 2030.

Memory is the purest expression of the trade. K3 activates less than 2% of its 2.8 trillion parameters per token, but every one of its 896 experts must sit resident in memory: 1.4TB before it serves a single request. Sparse models economize on FLOPs and gorge on capacity. Long context makes it worse — a 1M-token window is KV cache, and KV cache is memory. Verbosity makes it worse still: K3’s doubled token burn is decode-heavy work, and decode is bound by memory bandwidth, not compute. Open, sparse, long-context, token-hungry models are precisely the workload HBM was built for. The market is already pricing the squeeze: Bank of America puts the HBM market at $54.6B in 2026, up 58%, with DRAM revenue up 51% and total memory past $440B — and Microsoft attributed roughly $25B of its capex guidance to memory and component inflation alone. Margin gravity says the dollars pool at the scarcest physical constraint. In 2026 that constraint is not FLOPs. It is memory.

The geography is the under-priced part. Export controls mean Moonshot cannot serve global demand from Chinese silicon; it serves K3 today at a throttled ~26–28 tokens per second. Releasing the weights exports the serving demand to the only infrastructure that can absorb it: Western GPUs. The Sputnik analogy gets the consequences backwards. Sputnik was a rival’s closed capability. K3 is a demand shock delivered directly to American data centers.

Bullish: The Inference Companies

When the model is free, serving is the business

Inference providers are the direct monetization layer for open weights. They capture the serving revenue Moonshot gives up, and the private market has spent twelve months repricing them for it.

Fireworks closed a $1.5B Series D at $17.5B this week, up from $4B in late 2025, with ARR past $1B (5x YoY), daily token volume past 40T, and ~95% of tokens served on models fine-tuned from open weights. Together raised at $8.3B on more than $1.15B of bookings, serving open models exclusively. Baseten’s estimated ARR tripled to ~$600M in a single quarter. Nvidia agreed to pay ~$20B for Groq. Cerebras doubled on its IPO day.

Now watch the mechanism run in real time. K3 is currently served by exactly one provider: Moonshot itself. July 27 changes that. When K2.6’s weights opened, it hit #1 on OpenRouter with 1.88T tokens served in a week across roughly twenty competing hosts; when DeepSeek’s last flagship dropped, Fireworks listed it the same day. Hosts profitably served K2.7-class models (32B active parameters) at $4 per million output tokens. K3 activates 50B parameters and lists at $15. That spread is the auction’s opening bid, and competition will close it toward cost — margin that accrues to serving platforms and their GPU suppliers, not to Moonshot, which collects nothing and has already seeded vLLM with the attention kernels to accelerate its own disintermediation.

Who Wins & Why

The margin ledger, layer by layer

Call it margin gravity. In AI, margin flows down the stack until it pools at the scarcest physical constraint. Open frontier weights unbundle intelligence from the infrastructure that serves it — and what cannot be downloaded is gigawatts of contracted power, installed accelerators, serving economics won through utilization and kernels, and the enterprise control plane.

What to watch — five dated catalysts

July 27: the weights and the license. Confirmation of modified-MIT terms, and how fast third-party hosts light up. Precedent says same-day: Fireworks listed DeepSeek’s last flagship within hours of the drop.

A token-efficient open frontier model. Baker’s true Sputnik moment. K3 at $0.94/task vs. Grok 4.5 at $0.31 defines the gap; the first open model to close it ends the closed labs’ last economic argument below the frontier.

Grok 5, Composer 4, Muse 2 on the Pareto frontier. Vertical integration is the second road to model-layer margin compression. Multiple integrated players at multiple price-intelligence points would finish what open weights started.

The tokens-to-dollars gap. Open weights: 29% of gateway tokens, under 4% of spend. Each quarterly print that narrows it converts the token vote into revenue for inference providers and neoclouds — and out of lab pricing power.

How fast the labs become their own infrastructure. OpenAI’s 10GW Broadcom program and 6GW of AMD; Anthropic’s million TPUs and $30B Azure commitment. The faster the labs verticalize, the louder they are conceding that the model layer alone no longer carries the valuation.

The risk case is concentrated, not diffuse. Enterprise dollars stay closed longer than the token data implies — trust, liability, inertia. Washington moves: the House already probed Airbnb and Cursor’s parent over Chinese-model use, and restrictions in regulated sectors would slow adoption where the dollars are. Or a lab’s internal checkpoints compound into a lead nobody closes. Each slows the repricing. None reverses it, because the mechanism — margin flowing to the scarcest physical constraint — doesn’t depend on which model wins.

The weights are free. The gravity is not.